Trying to time the stock market is infamously risky, with most investors failing to profit from it in the long run. Usually, these investors try to reap short – term gains by attempting to predict market movement. This strategy is very risky in nature, however, most particularly during times of market volatility.

Volatility is both normal and expected when investing, especially in the short term. An easy way to manage these bumps in the road is by investing for the long term, which allows investors to stay calm and ride out temporary dips until the market inevitably rebounds. It can also lead to higher returns: according to Forbes, over a 20- year period, 90% of passive index funds tracking companies outperformed their active counterparts.

A systematic investment plan for the long term, or dollar cost averaging, is a strong approach for building wealth over time while getting through volatility. Here’s what you need to know about dollar-cost averaging and how it can help you maximize your investment gains and stay aligned with your long term investing strategy.

Dollar-cost averaging is the practice of investing the same amount of money on a regular, recurring basis. Many investors ensure their budgets allow them to invest automatically on a weekly, monthly and/or quarterly basis. This allows then to stay in line with their plan and practice good investing habits.

Dollar-cost averaging works because volatility is always a factor in the stock market. Prices will move up or down in response to macroeconomic factors, news, and other externals, as you may have seen in the economic impact of the Russia-Ukraine conflict and rising inflation rates. Over time, however, the market has always rebounded from crashes and moved higher. This was most evident during the Covid-19 pandemic; the market picked back up after the initial crash and those who stayed the course and continued investing through the dip achieved better gains and results. Dollar-cost averaging allows you to continue investing during downturns in the market, during which your money will buy more shares of your chosen stock or index due to the discounted prices. Over time, this protects your portfolio from losses while allowing you to take advantage of gains made during rebounds.

This strategy also helps to protect you from risks inherent in trying to time the market. Investors who use recurring deposits to average their cost basis are less likely to buy and sell . Instead, they can continue to invest the same amount each month and allow the market to work for them. Investors who try to time the market, by contrast, often buy or sell at the wrong time and lose out on potential gains. Market timing is extremely difficult, and very few investors will get it right consistently over multiple decades.

Finally, dollar-cost averaging lets you take advantage of by putting your money to work immediately rather than waiting for a buying opportunity. The average lasts nearly four years. An investor who waits that long to buy misses out on the gains produced by the bull market. The investor who practices dollar-cost averaging, by contrast, can take advantage of compounding gains while the bull market lasts, then benefit from discounted stock prices when the market recedes. Over time, this will produce greater gains than holding cash and waiting for a chance to buy low.

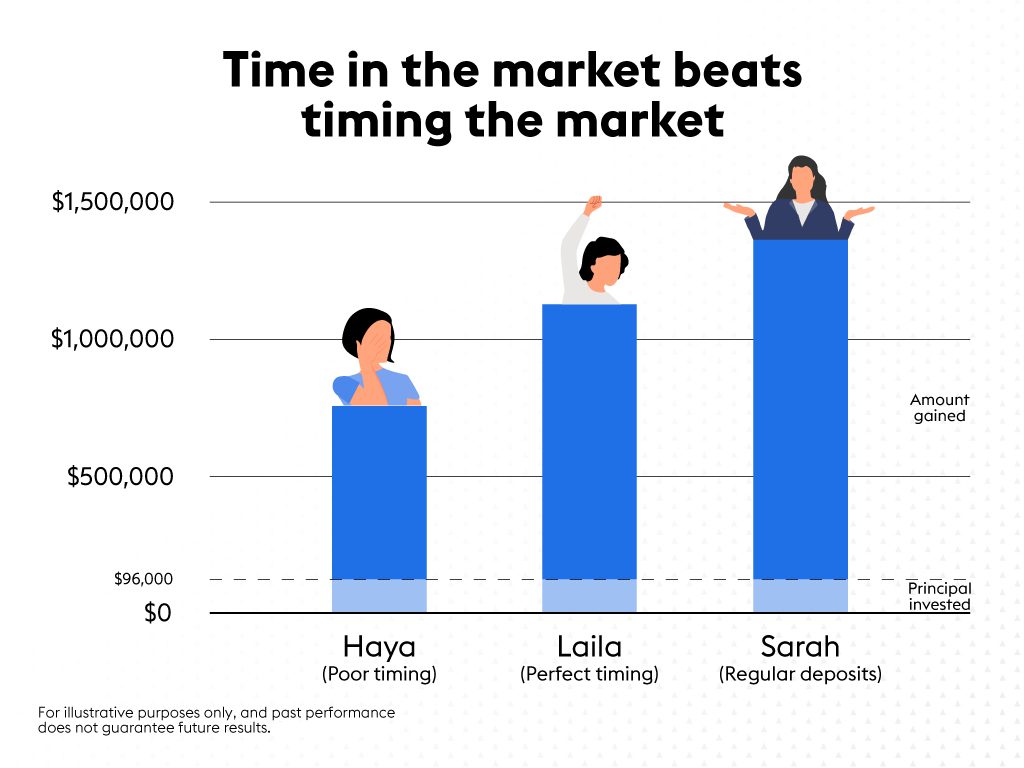

Now that we’ve seen the power of dollar-cost averaging, let’s examine some hypothetical case studies that show just how effective it can be. Here are three examples of people with different strategies (who invested from 1982 to 2022) to show exactly how dollar-cost averaging benefits investors over the long run.

- Haya

Haya had $96,000 to invest and always bought at the absolute top of the market. Haya has the worst-case scenario because her cost basis is consistently high, and she never manages to take advantage of discounted prices. Haya never sells, allowing rising markets to compensate for her higher costs. By the time she retires, Haya has gained $764,000 for a total portfolio value of $860,000. Her strategy of buying and holding allowed her to see good results over time.

- Laila

Laila is Haya’s opposite, always investing at the bottom of the market. Like Haya, she had $96,000 to invest and never sold her shares. Haya and Laila retire at the same time. Because she bought when stocks were cheap, Laila retires with $1,128,332, about 31 percent higher than Haya’s final total. Laila has a more cost-effective strategy than Haya, as she used the buy-hold strategy and took advantage of the market downturn and discounted prices.

- Sarah

The third investor, Sarah, takes a fundamentally different approach. Beginning in 1982, Sarah has deposited $200 per month into her investment account. Because Sarah’s deposits happen monthly, she has bought into both the best and worst days of the market over time. This long-term strategy allowed her to gain $1,366,320, resulting in a total portfolio value of $1,462,320. Over this period, her monthly deposits totaled $96,000, exactly the same as Laila and Haya. Sarah has the most powerful strategy as she has stuck to her long-term investing strategy that allowed her to navigate any market volatility, whilst still achieving gains.

Why did Sarah’s strategy outperform both of the other two investors? In Haya’s case, it’s a simple matter of cost basis. Sarah invested at both market highs and market lows, allowing her to take advantage of discounted prices during downturns.

Laila’s case is a bit more complicated. Because Laila waited to time the market and bought only during downturns, she often had to wait to invest. During bull markets, Laila’s money was sitting in cash and not producing returns. Sarah’s money, by contrast, went directly into the market and grew as a result of compounding interest. Over time, Sarah’s consistent investing overtook Laila’s lower cost basis because money invested early in Sarah’s life had more time to grow.

As you can see, dollar-cost averaging over long periods outperforms attempts to time the market.

If you’re interested in leveraging the power of passive dollar-cost averaged investing in your own investments, consider using the NBK Capital SmartWealth to help you achieve your financial goals.